State minimum coverage costs 30–50% less per month than full coverage, but you could face $20,000+ out-of-pocket costs after a single crash. Here's how to decide if minimum limits are worth the risk.

The Real Cost Gap Between Minimum Coverage and Actual Crashes

You're looking at your renewal notice or shopping for your first policy, and the price difference is staring back at you: state minimum coverage might run $45–$65 per month, while full coverage with higher limits costs $110–$150 per month. That $50–$85 monthly savings feels significant, especially if you've never filed a claim.

But state minimum liability limits haven't kept pace with actual crash costs. The most common minimum bodily injury limit is $25,000 per person, yet the average non-fatal injury crash costs $42,000 in medical bills and lost wages, according to NAIC data. Property damage minimums in many states sit at $10,000 or $15,000, while the average vehicle on the road today is worth $28,000. If you cause a crash that exceeds your limits, you pay the difference out of pocket — and that liability doesn't disappear in bankruptcy in most states.

The decision isn't whether minimum coverage is legal. It's whether you can absorb a $20,000–$50,000 personal liability if your $25,000 bodily injury limit runs out after hitting another driver who needs surgery. For drivers with minimal assets, wages subject to garnishment, or any property to protect, minimum limits create a direct financial exposure that monthly premium savings rarely justify. liability insurance

What State Minimum Actually Covers — And Where It Fails

State minimum policies typically include liability-only coverage: bodily injury liability and property damage liability. These pay for harm you cause to others, but they pay nothing for your own vehicle, your own injuries, or damage caused by uninsured drivers. In the 30 states with minimum bodily injury limits at or below $25,000 per person, you're covered for minor crashes — fender benders with soft tissue injuries and older vehicles.

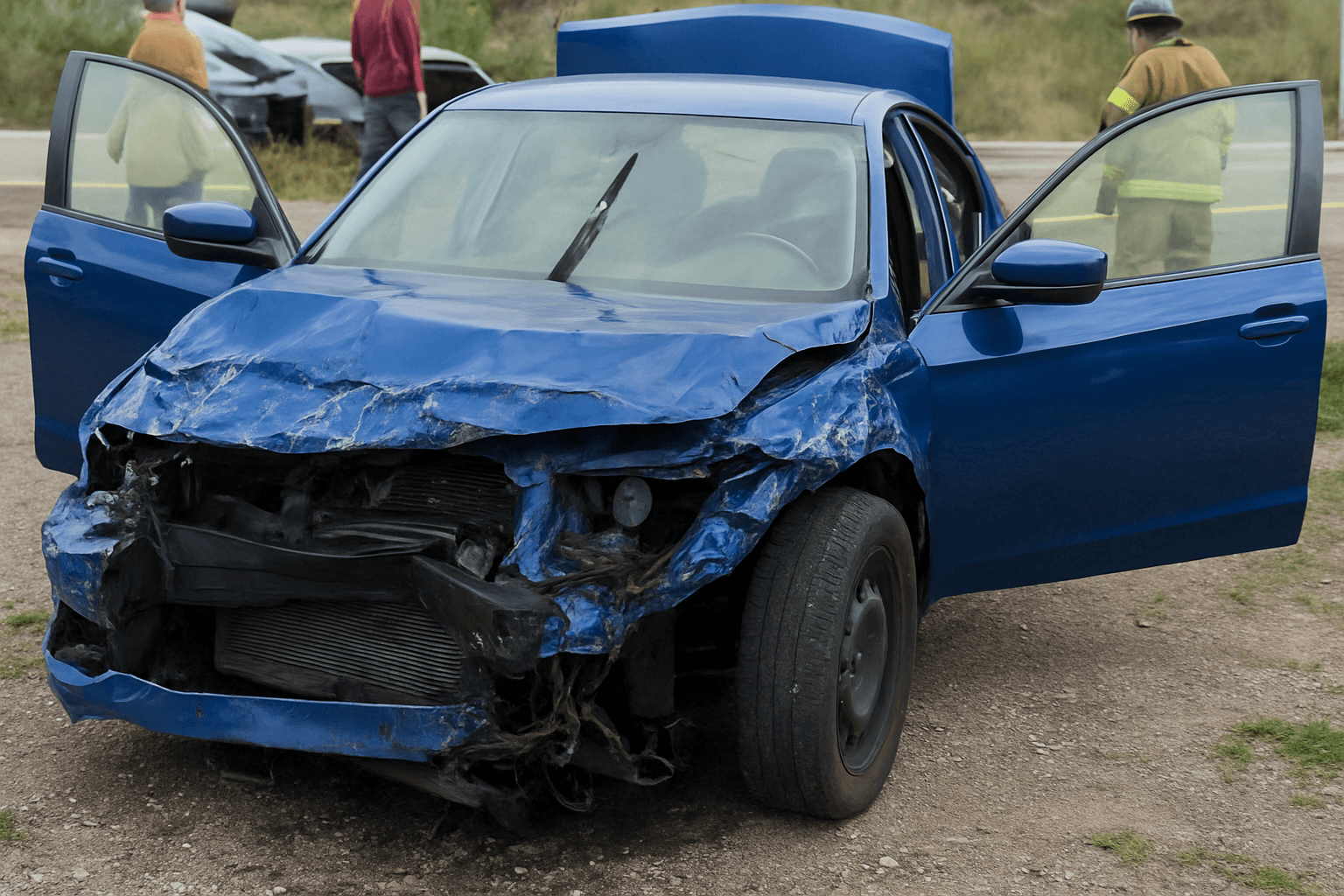

The gap appears in moderate crashes. A two-car accident with airbag deployment, a broken bone, and vehicle damage to a late-model SUV can easily generate $60,000 in combined costs. Your $25,000/$50,000 bodily injury limit and $25,000 property damage limit cover $50,000 at most if two people are injured. You're personally liable for the remaining $10,000, plus your own vehicle repair costs, plus your own medical bills if you're injured.

Minimum coverage also excludes collision and comprehensive coverage, which means any damage to your own vehicle — whether from a crash you cause, a hit-and-run, weather, theft, or vandalism — is entirely your responsibility. If you're driving a vehicle worth more than $5,000, this creates a single-incident risk that can exceed a year's worth of premium savings. Drivers who choose minimum coverage often do so while driving older vehicles with minimal market value, which reduces but doesn't eliminate the financial exposure.

Compare auto insurance rates in your state

Get matched with licensed carriers in minutes. One short form, real quotes, no obligation.

Get Your Free Quote✓ Free to Compare✓ No Obligation✓ Licensed Carriers✓ TCPA Compliant

When Minimum Coverage Might Make Sense

Minimum coverage works for a narrow set of circumstances, not as a default budget choice. It's most defensible when you're driving a vehicle worth less than $3,000, have no significant assets or wages to protect, and can replace your vehicle out of pocket without financial hardship. This typically applies to drivers with older paid-off cars, minimal savings, and income below garnishment thresholds in their state.

Even in that scenario, the liability exposure remains. If you cause a serious crash, your lack of assets today doesn't shield you from judgments that can follow you for years. Some states allow wage garnishment for up to 25% of disposable income, and judgment collection periods can extend 10–20 years depending on state law. A $40,000 judgment on minimum wage income still extracts thousands of dollars over time.

The more defensible middle ground for budget-conscious drivers is increasing liability limits to $100,000/$300,000 while keeping collision and comprehensive coverage off the policy. This typically adds $15–$25 per month compared to state minimums but reduces catastrophic personal liability risk by 75–80%. You still pay for your own vehicle damage, but you're not facing potential bankruptcy from injuring another driver.

The Hidden Costs of Choosing Minimum Coverage

Beyond direct crash liability, minimum coverage creates secondary costs that don't appear on the policy declarations page. Many lenders require collision and comprehensive coverage for financed or leased vehicles, which makes minimum liability-only coverage unavailable unless you own your car outright. Drivers who try to reduce coverage on a financed vehicle trigger lender-placed insurance, which costs 2–4 times more than standard coverage and provides minimal protection.

If you're hit by an uninsured driver — which happens in approximately 13% of crashes nationally and exceeds 25% in some states — your minimum liability policy pays nothing for your injuries or vehicle damage. Uninsured motorist coverage, which handles this scenario, is excluded from most minimum policies or available only as an add-on. The out-of-pocket cost for a crash caused by an uninsured driver often exceeds $10,000 when you account for medical bills, lost wages, and vehicle repair.

Gap coverage also disappears with minimum policies. If you owe $18,000 on a vehicle worth $14,000 and total it in an at-fault crash, your liability-only policy pays nothing. You're responsible for the full $18,000 loan payoff plus the cost of replacing your transportation. This scenario is common in the first 2–3 years of a vehicle loan, when depreciation outpaces principal payments.

How to Decide: The Break-Even Framework

The actual decision point isn't monthly cost — it's whether you can cover the financial gap if minimum limits aren't enough. Calculate the difference between your state's minimum liability limits and realistic crash costs in your area. For most states, this gap sits between $15,000 and $50,000 for a moderate two-car injury crash. Ask whether you could pay that amount out of pocket without losing your home, draining retirement accounts, or facing wage garnishment.

If the answer is no, minimum coverage transfers that risk to you personally for a monthly savings of $50–$85. The break-even point is typically 4–8 months of premium savings compared to a single moderate crash. Drivers who maintain minimum coverage for years without a claim come out ahead financially — but only if they avoid crashes entirely. One at-fault injury crash in a 5-year period eliminates the cumulative savings and adds $20,000–$50,000 in personal liability.

For drivers who decide minimum coverage is still the right choice, prioritize increasing liability limits before adding physical damage coverage. Bodily injury liability at $100,000/$300,000 and property damage at $50,000 costs significantly less than adding collision and comprehensive coverage, but it addresses the liability risk that can follow you for decades. Physical damage coverage protects your vehicle; liability coverage protects your financial future.

What to Do If You're Already Carrying Minimum Coverage

If you're currently insured at state minimums and reconsidering your limits, request a quote with increased liability coverage before your next renewal. Most carriers allow mid-term policy changes, and the incremental cost to raise bodily injury limits from $25,000/$50,000 to $100,000/$300,000 typically adds $15–$30 per month depending on your state and driving record. This change takes effect immediately and eliminates the largest financial exposure.

If budget constraints make any increase difficult, focus on liability first and physical damage second. Collision and comprehensive coverage protect your vehicle, but liability coverage protects everything else you own. A driver with a $4,000 car and $30,000 in savings is better served by higher liability limits and no collision coverage than by keeping minimum liability and adding collision. The vehicle is replaceable; a $60,000 injury judgment is not.

Drivers who've already been in an at-fault crash while carrying minimum coverage should verify whether their liability limits fully covered the claim. If the other party's damages exceeded your policy limits, you may have personal exposure even if the claim appeared settled. Contact your insurer to confirm whether any excess liability exists, and consult an attorney if you've received demand letters or notice of judgment. Some states allow negotiated settlements that reduce personal liability, but only if addressed before judgments are finalized. Compare quotes